How to Manage Unexpected Retirement Expenses

What is the true cost of retirement and what are the driving forces behind unexpected and expected retirement expenses?

Whether you plan to globetrot or enjoy life at home in retirement, your main goal is likely not running out of money. In order to live the life you hope with the income you have, consider developing a budget that accounts for planned and unplanned retirement expenses.

Over time, how we spend money changes, so as you develop your plan it is important to assess what costs may go up, what costs may go down (or away), and what factors are driving these costs. Many retirees can expect to spend less in certain areas. For example, in retirement the costs associated with commuting diminishes and the demand for multiple cars and/or high-end cars may lessen.

However, those new found savings can be offset by unexpected costs that come with retirement life. As we enjoy longer, healthier retirements, it becomes more and more difficult to budget for one-time travel plans. From a grandchild's graduation to a long-time friend's wedding anniversary, there will be unexpected adventures you do not want to miss.

Retirement Expense Solutions

Retirement planning would be easier without surprises. While we cannot anticipate every unexpected retirement expense, we can prepare for them. As your plan develops, establish retirement income solutions that help you manage unanticipated line items, such as:

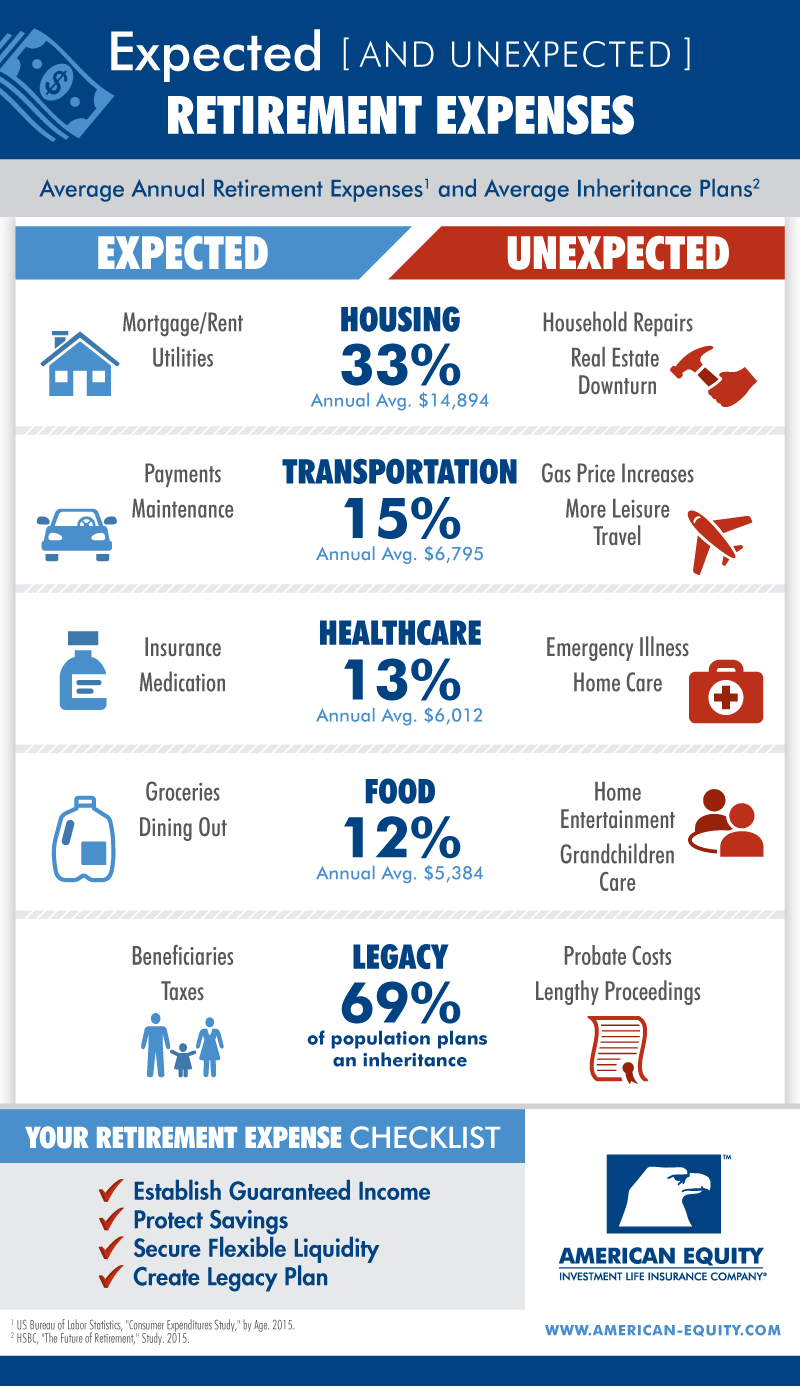

- Establish Guaranteed Income Stream

- Protect Hard-Earned Savings

- Secure Safe-Money Reserve Access

- Create Legacy Plan

To demonstrate where these solutions can benefit your retirement, below we highlight five common types of real life retirement expenses. Included are the average annual spending amounts for retirees and the average inheritance figures, according to the US Bureau of Labor Statistics and an HSBC retirement study. In each instance, we outline examples of expected and unexpected cost factors to consider as you prepare for your retirement future.

Everyone's retirement priorities and lifestyles differ. By starting with universal demands like savings protection, a guaranteed revenue stream and flexible income, anyone can develop the foundation of a retirement spending plan that accounts for what may lie ahead.

The true costs of retirement will never be totally fixed, but there are ways to make unexpected costs less stressful. As you plan your own retirement spending, focus less on what could happen and more on what strategies can be put in place for whatever happens.

Sources:

US Bureau of Labor Statistics, "Consumer Expenditures Study," by Age. 2015HSBC, "The Future of Retirement," Study. 2015

The information provided is for educational purposes only and does not constitute advice. For specific details on how this may apply to your personal situation contact your personal financial advisor or insurance agent for more details. American Equity contracts are only sold through independent agents. Please contact our home office Agency Services department at (888) 221-1234 option 3, or your state insurance department, to see if there is an independent insurance agent in your area appointed to sell American Equity annuity contracts. US Bureau of Labor Statistics, "Consumer Expenditures Study," by Age. 2015HSBC, "The Future of Retirement," Study. 2015

Sourced From: American Equity

https://www.american-equity.com/resources/blog/how-to-manage-unexpected-retirement-expenses

Comments

Post a Comment